Online lending apps in the Philippines often request access to sensitive phone features during registration. Some permissions support legitimate identity verification and fraud prevention, while others can expose borrowers to privacy abuse, coercive collection tactics, spam, contact harassment, or unauthorized data harvesting. Borrowers searching for “dangerous loan app permissions Philippines” should carefully review requests for contact access, SMS permissions, gallery access, camera permissions, microphone use, location tracking, and device fingerprinting before approving them.

Legitimate lenders usually request only the minimum permissions needed for KYC verification, fraud checks, and loan servicing. Excessive or unrelated permissions may indicate aggressive collection practices or weak privacy controls. Reviewing app permissions before installation helps reduce risks involving contact shaming, identity misuse, and invasive tracking behaviors that have affected many digital lending users in the Philippines.

Summary:

Loan apps in the Philippines sometimes request invasive permissions that go beyond normal lending verification. High-risk permissions include contact access, SMS reading, photo gallery access, microphone permissions, device tracking, and continuous location monitoring. While SEC-compliant lenders may request camera access for KYC and limited device verification for fraud prevention, excessive permission requests can expose borrowers to harassment, privacy abuse, spam collection tactics, and personal data misuse. Before borrowing, users should review every permission carefully, minimize access whenever possible, verify lender legitimacy, and compare the app’s requested permissions with its actual lending function. Privacy-conscious borrowing reduces both financial and digital security risks.

Why Loan App Permissions Matter More Than Most Borrowers Realize 📱

Many borrowers focus only on approval speed, loan limits, and repayment terms. However, app permissions can quietly determine how much personal information a lender can collect long after installation.

In the Philippine digital lending market, mobile onboarding has become heavily automated. Apps may request:

- Camera access for ID verification

- SMS permissions for OTP detection

- Contact access for referral or identity checks

- Location tracking for fraud prevention

- Device information for risk scoring

Some of these requests are operationally reasonable. Others are excessive.

Problems begin when lending apps combine large-scale data collection with aggressive collection behavior. Borrowers who miss payments sometimes report:

- Contacts receiving spam messages

- Threatening reminders sent through multiple channels

- Personal photos being referenced during collection

- Persistent tracking notifications

- Unauthorized marketing campaigns

This is why permission review is now part of safe borrowing behavior, not just cybersecurity hygiene.

Borrowers researching SEC registered loan apps Philippines should also evaluate how much personal data an app wants before approving access.

The Most Dangerous Loan App Permissions Borrowers Should Watch Closely

Contact Access: The Highest-Risk Permission for Harassment

Many borrowers ask: “Why do loan apps ask for contacts?”

Some lenders claim contact access helps:

- Verify identity consistency

- Detect fraud rings

- Support emergency contact validation

However, abusive lenders have historically used contact lists for coercive collection practices.

When borrowers grant contact permissions, apps may potentially access:

- Family members

- Co-workers

- Clients

- Business partners

- School contacts

- Religious or community groups

If repayment problems occur, unethical operators may pressure borrowers through social embarrassment tactics.

This is one reason Philippine regulators and privacy advocates have repeatedly warned against excessive data collection by digital lenders.

What Responsible Lenders Usually Do Instead

More privacy-conscious lenders now:

- Request manually entered references

- Limit contact collection

- Avoid automatic phonebook syncing

- Use consent-based verification flows

A legitimate app should clearly explain:

- Why contact access is needed

- Whether data is stored

- How long data is retained

- Whether access is optional

If a loan app refuses to proceed unless full contact syncing is enabled, borrowers should proceed carefully.

Loan App Contact Permission Risk Warning Philippines

(Loan app requesting contact access on Android phone with borrower privacy risk warning)

SMS Permissions: Useful or Excessive?

SMS permissions are common in digital lending apps because many platforms automate OTP verification.

Legitimate uses include:

- Reading one-time passwords automatically

- Confirming linked mobile numbers

- Detecting fraud patterns tied to SIM activity

However, broad SMS access may expose:

- Banking notifications

- E-wallet alerts

- Salary messages

- Personal conversations

- Transaction histories

Some apps may use SMS-derived financial patterns for alternative credit scoring.

For example, lenders may analyze:

- Frequency of incoming transfers

- E-wallet usage behavior

- Telecom payment consistency

- Financial notification patterns

While alternative scoring is increasingly common in fintech, borrowers should question whether full SMS access is proportionate to the loan amount being requested.

When SMS Permissions Become a Red Flag

Be cautious if:

- The app requests permanent SMS access

- Permission explanations are vague

- SMS reading seems unrelated to verification

- The lender lacks clear privacy disclosures

Borrowers concerned about abusive behavior should also learn about borrower harassment protections before sharing sensitive permissions.

Can Loan Apps Read Your Photos and Gallery Files?

Gallery Access and ID Photo Risks

Many loan apps ask for gallery access to:

- Upload IDs

- Submit proof of billing

- Attach income documents

This is operationally normal during digital KYC.

However, unrestricted gallery permissions may expose:

- Personal family photos

- Screenshots

- Financial records

- Private documents

- Work-related files

Some borrowers worry about ID photo misuse after uploading sensitive identification images.

That concern is reasonable because identity documents often contain:

- Full legal name

- Birth date

- Address

- Signature

- ID numbers

Combined with device data and contact information, this creates a large personal data footprint.

Safer Borrowing Practices for Document Uploads

Borrowers can reduce risk by:

- Uploading files only during application

- Revoking permissions afterward

- Using a separate folder for lending documents

- Avoiding unnecessary gallery-wide access

- Reviewing Android permission settings manually

Modern Android systems increasingly support “selected photos only” access instead of full gallery access. This is usually safer than granting unrestricted permissions.

Camera Access: Often Legitimate but Still Sensitive

Is camera access normal?

In most SEC-compliant digital lending workflows, yes.

Camera access is commonly used for:

- Selfie verification

- Facial matching

- Liveness detection

- ID capture

- Fraud prevention

These checks support anti-fraud compliance and remote onboarding.

However, borrowers should still evaluate:

- Whether camera access is active only during verification

- Whether the app explains biometric handling

- Whether privacy disclosures mention retention periods

Apps that request continuous background camera permissions without clear explanation deserve additional scrutiny.

Safe vs Dangerous Loan App Permissions Comparison

(Comparison chart showing safe lending app permissions and dangerous invasive permissions)

Device Fingerprinting and Tracking: The Hidden Layer Most Users Miss

What Is Device Fingerprinting?

Device fingerprinting refers to collecting unique technical identifiers from a phone or device.

Loan apps may gather:

- Device model

- Operating system version

- IP address

- SIM details

- Installed app patterns

- Behavioral signals

- Login consistency

Legitimate lenders use these signals to:

- Detect fraud

- Prevent duplicate accounts

- Reduce identity theft

- Identify suspicious activity

This has become common in Philippine fintech risk assessment systems.

When Tracking Becomes Excessive

Problems arise when apps:

- Collect unrelated behavioral data

- Track users continuously

- Combine multiple invasive permissions

- Share information with unclear third parties

Borrowers should carefully review:

- Privacy policies

- Data-sharing disclosures

- App store reviews

- NPC-related complaints

- Permission lists before installation

Apps requesting unusually broad access may fit patterns associated with aggressive operators or weak compliance culture.

Location Permissions: Sometimes Necessary, Sometimes Excessive 📍

Why Some Lenders Request Location Access

Location access may support:

- Fraud detection

- Identity consistency checks

- Regional service eligibility

- Anti-scam verification

For example, lenders may compare:

- IP location

- Device location

- Declared address

Large inconsistencies can trigger manual review.

Continuous Location Tracking Is Usually Unnecessary

Most lending apps do not need:

- 24/7 GPS tracking

- Background location monitoring

- Constant movement history

Borrowers should prefer:

- “Allow only while using the app”

- One-time location access

- Approximate location sharing where possible

If an app requires permanent background tracking to process a small consumer loan, that deserves caution.

How Permission Abuse Connects to Collection Harassment

One major reason this topic matters in the Philippines is the historical link between invasive permissions and collection abuse.

Apps with excessive access may potentially use:

- Contact lists

- Social networks

- Messaging data

- Device information

- Photos or identifiers

to pressure borrowers after missed payments.

Common borrower complaints historically associated with abusive operators include:

- Text blasts to contacts

- Embarrassing debt messages

- Threats involving public exposure

- Repeated harassment calls

- Social intimidation tactics

This is why permission minimization matters even before borrowing begins.

Users comparing lenders should not rely solely on marketing claims. It is also important to verify SEC compliant loan apps before sharing sensitive information.

Android Permission Categories Borrowers Should Review Carefully

High-Risk Permissions

These permissions deserve extra caution:

| Permission | Potential Risk |

|---|---|

| Contacts | Harassment targeting family or co-workers |

| SMS | Access to financial notifications |

| Storage/Gallery | Exposure of personal files |

| Microphone | Privacy concerns if misused |

| Background Location | Continuous tracking |

| Call Logs | Contact behavior profiling |

Lower-Risk Operational Permissions

These are often more reasonable:

| Permission | Common Legitimate Purpose |

|---|---|

| Camera | ID verification |

| Notifications | Payment reminders |

| Limited Location | Fraud prevention |

| Biometric Login | Account security |

The key question is proportionality.

A small emergency loan app should not require broader access than necessary to verify identity and manage repayment.

What the National Privacy Commission (NPC) Has Warned About

The National Privacy Commission has repeatedly emphasized:

- Transparency in data collection

- Purpose limitation

- Consent clarity

- Responsible handling of personal information

Borrowers should pay attention to:

- Permission popups

- Consent wording

- Data retention statements

- Third-party sharing disclosures

Apps that hide important privacy details inside vague legal language may increase user risk.

Signs a Loan App May Be Collecting Too Much Data 🚨

Warning Signs Before Installation

Be cautious if:

- The app asks for nearly every phone permission immediately

- Permission explanations are unclear

- Reviews mention harassment or spam

- The privacy policy is vague or missing

- The app pressures users to enable all permissions

- Access requests seem unrelated to lending

Behavioral Red Flags After Installation

Some users notice:

- Sudden marketing spam

- Frequent background activity

- Battery drain from tracking behavior

- Contacts receiving promotional texts

- Excessive notifications

These patterns do not automatically prove abuse, but they justify closer review.

Borrowers evaluating questionable platforms should also learn common fake lender warning signs before proceeding.

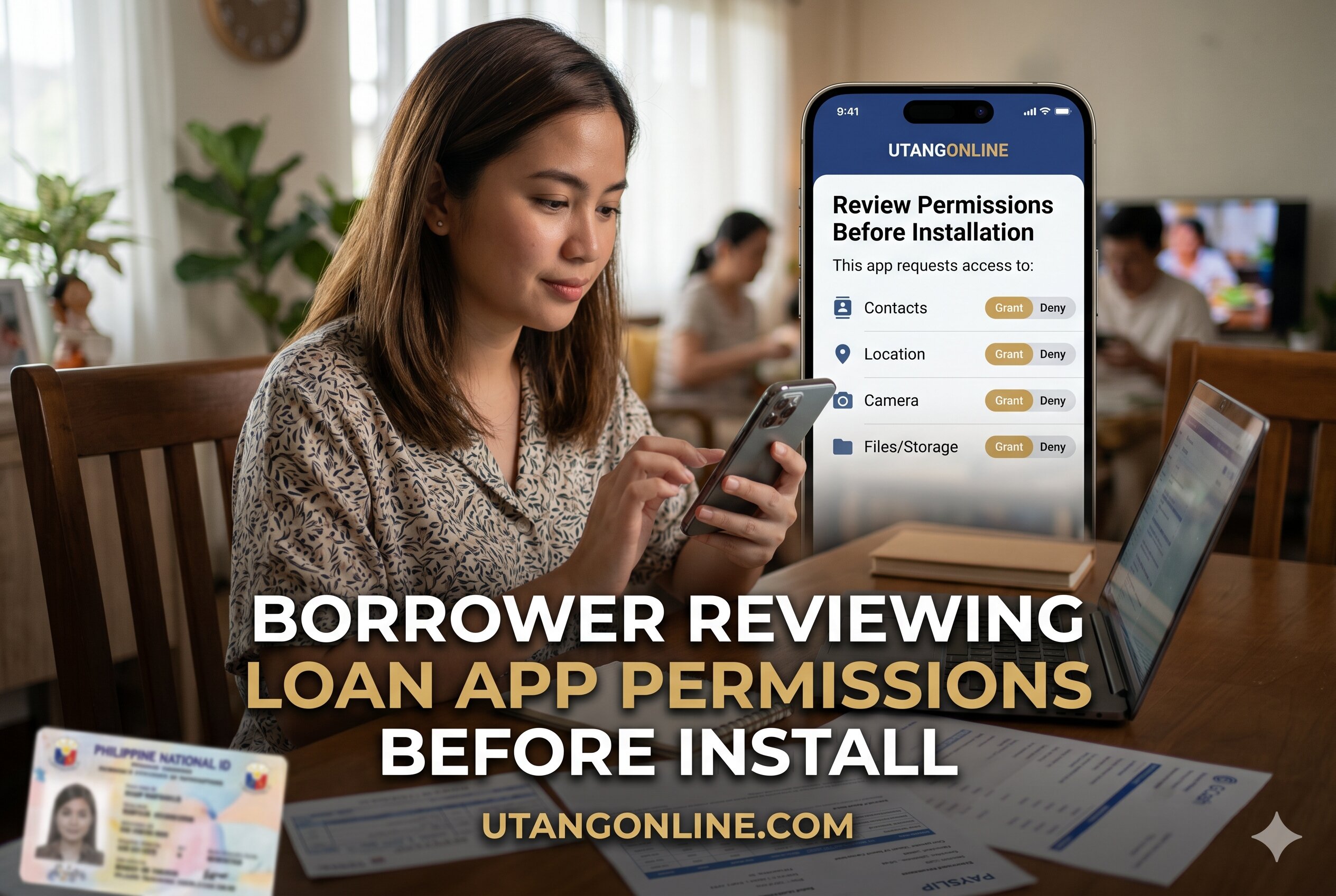

Borrower Reviewing Loan App Permissions Before Install

(Philippine borrower checking Android loan app permissions before approving installation)

How SEC-Compliant Lenders Usually Handle Permissions

More Mature Compliance Practices

Better-regulated lenders often:

- Explain permission requests clearly

- Limit unnecessary access

- Separate KYC from marketing permissions

- Allow partial functionality without broad tracking

- Maintain clearer privacy disclosures

They also tend to align more closely with:

- Data privacy expectations

- Responsible collection practices

- Consent documentation

- Risk-based verification

Why Legitimate Apps Still Need Some Data

Borrowers should avoid assuming every permission is abusive.

Modern digital lending systems require some data to:

- Prevent synthetic identity fraud

- Detect account takeovers

- Validate applicant authenticity

- Reduce fake applications

- Support remote onboarding

The issue is not whether permissions exist. The issue is whether the permissions are excessive relative to the lending function.

Practical Permission Safety Checklist Before Applying ✔️

Before installing a loan app:

- Review permissions before tapping “Allow”

- Compare requested access with the app’s purpose

- Avoid apps demanding full contact syncing

- Check app reviews for harassment complaints

- Read the privacy policy carefully

- Revoke unused permissions after approval

- Use updated Android privacy controls

- Avoid sharing unnecessary gallery access

- Confirm SEC-related legitimacy claims

- Monitor suspicious activity after installation

Borrowers using multiple lending apps should regularly audit phone permissions because unused apps may still retain access.

FAQs About Dangerous Loan App Permissions in the Philippines

Why do loan apps ask for contacts?

Some lenders claim contact access helps with fraud prevention and reference verification. However, abusive operators have historically used contact data for coercive collection tactics and social pressure campaigns.

Is camera access normal for lending apps?

Yes. Camera permissions are commonly used for digital KYC, ID capture, selfie verification, and liveness checks. Legitimate apps usually activate camera access only during verification steps.

Should I allow SMS permissions?

Limited SMS permissions for OTP detection may be reasonable. Full SMS access that allows reading financial notifications and personal messages deserves careful review.

Can loan apps read my photos?

Apps with gallery or storage permissions may potentially access photos and stored files depending on the permission scope. Borrowers should prefer limited-access settings whenever possible.

Can SEC-registered lenders still request invasive permissions?

Yes. SEC registration does not automatically guarantee ideal privacy practices. Borrowers should still evaluate permissions carefully and review privacy disclosures independently.

What should I do if I already granted dangerous permissions?

You can:

- Revoke permissions in Android settings

- Delete unused apps

- Change sensitive passwords

- Monitor suspicious activity

- Review privacy settings regularly

Conclusion

Loan app permissions are no longer a minor technical detail in the Philippine lending ecosystem. They directly affect borrower privacy, digital security, and even collection experience.

Some permissions are operationally reasonable because modern fintech onboarding relies on remote identity verification, fraud detection, and automated KYC workflows. However, excessive access requests involving contacts, SMS data, galleries, device tracking, or continuous monitoring can expose borrowers to unnecessary risks.

Before applying, borrowers should evaluate both the lender’s legitimacy and its data collection behavior. Responsible borrowing now includes permission awareness, privacy-conscious app management, and careful review of how personal information may be used after installation.

A fast loan approval should never require surrendering more personal data than necessary.

Last Updated on May 18, 2026 by Michael Reyes