Installing a lending app in the Philippines takes only a few minutes. Recovering from identity theft, abusive collections, or fake debt claims can take months. Many borrowers assume that if an app appears on the Google Play Store or Apple App Store, it is automatically legal. That assumption creates risk.

A legitimate online lender in the Philippines should have a registered business entity and proper authority connected to lending operations. Some apps operate under different brand names, use misleading company identities, or continue collecting payments even after app store removal. Before uploading IDs, selfies, payroll details, or contact permissions, borrowers should verify the lender through multiple regulatory and operational checks.

Summary:

To verify how to verify sec registered loan apps philippines, borrowers should match the loan app name with the legal company entity, check the company through the SEC database, review the lender’s website disclosures, compare app store information, and inspect complaint patterns and permissions behavior. A legitimate lender normally discloses its corporate name, SEC registration details, privacy policies, and contact information consistently across its app listing and website. Borrowers should avoid APK-only downloads, apps requesting excessive phone permissions, and lenders that hide their corporate identity. Verification helps reduce scam exposure, protects personal data, and lowers the risk of harassment or fraudulent collections.

Why SEC Verification Matters Before Installing a Loan App

The Philippine digital lending market expanded rapidly because of mobile-first borrowing, e-wallet adoption, and simplified KYC onboarding. Many Filipinos now apply for loans using only a smartphone, government ID, and selfie verification.

That convenience also created opportunities for fraudulent operators.

Some apps:

- Use fake company names

- Clone legitimate lenders

- Operate without proper authorization

- Harvest personal contacts and gallery data

- Disappear after collecting borrower information

- Continue debt collection through unofficial channels

A borrower who verifies a lender first is not only checking legality. They are also checking operational credibility, data handling behavior, and regulatory visibility.

This is especially important for:

- First-time borrowers

- Freelancers and gig workers

- Users applying through Facebook ads or SMS links

- People receiving APK download invitations

- Borrowers pressured into immediate application submission

The safest habit is simple: verify first, install later.

What “SEC Registered” Actually Means for Loan Apps

Many borrowers misunderstand the phrase “SEC registered.”

A company being registered with the Philippine Securities and Exchange Commission does not automatically mean it is legally operating as a lending platform. Some companies are merely incorporated businesses without lending authority.

Borrowers should distinguish between:

- Business incorporation

- Lending authority

- Online lending operation disclosures

Corporate Registration vs Lending Authority

A business may legally exist as a corporation but still lack authority to conduct lending activities.

Legitimate lending operations normally disclose:

- Corporate name

- SEC registration number

- Certificate of Authority details

- Registered office address

- Contact channels

- Privacy policies

This is why simply seeing a business name inside an app listing is not enough.

Why App Names and Company Names Often Differ

One major source of borrower confusion is entity mismatch.

Example:

- App Name: “FastCash PH”

- Legal Company: ABC Financing Corporation

This is common in the Philippine fintech industry because brands operate separately from corporate entities.

Borrowers should always trace:

- The app brand

- The website entity

- The SEC-listed company name

- The privacy policy operator

If these names do not align, further checking is necessary.

Step-by-Step Verification Workflow ✅

This section answers the core search intent directly.

Step 1: Identify the Exact Company Behind the App

Before checking the SEC database, identify the legal entity operating the app.

Look inside:

- Google Play Store listing

- Apple App Store profile

- Privacy policy

- Terms and conditions

- Official website footer

- Contact page

Legitimate lenders usually display:

- Full corporate name

- Office address

- Email support

- Registration disclosures

Red flag signs include:

- No company name

- Generic Gmail addresses

- No website

- Broken privacy policy links

- Only Telegram or Facebook contact details

SEC Loan App Verification Workflow Philippines

(Step-by-step process for verifying SEC registered loan apps in the Philippines using app stores and SEC records)

Step 2: Search the SEC Database

The next step is entity matching.

Borrowers should search the company name exactly as written in the lender disclosure.

Important checks:

- Does the company exist?

- Is the spelling identical?

- Is the status active?

- Does the entity type match lending operations?

This matters because scam apps sometimes:

- Copy names of inactive corporations

- Slightly alter legitimate company names

- Use unrelated registered entities

Search carefully when:

- Words are abbreviated

- “Corporation” or “Inc.” is omitted

- Multiple similar names appear

A legitimate fintech company normally maintains naming consistency across:

- App stores

- Website disclosures

- Privacy documents

- Customer support communications

How to Cross-Check App Store Information

Many borrowers stop after seeing an app on the Play Store. That is not enough.

Are Play Store Apps Automatically Legal?

No.

App stores remove malicious apps regularly, but approval into the marketplace does not guarantee Philippine regulatory compliance.

Some illegal lenders temporarily appear on app stores before complaints accumulate.

Borrowers should inspect:

- Developer identity

- Number of downloads

- Review patterns

- Permission requests

- Update frequency

- Website consistency

A sudden flood of generic 5-star reviews can also indicate manipulated ratings.

Warning Signs Inside App Listings

Common warning indicators include:

- No identifiable company

- Excessive permissions requests

- APK-only installation instructions

- Broken support email addresses

- No privacy policy

- Pressure-based marketing claims

- Unrealistic approval promises

Apps claiming:

- “Guaranteed approval”

- “Instant cash regardless of credit”

- “No verification needed”

should be reviewed carefully.

Responsible lenders still conduct risk assessment, KYC checks, and fraud screening.

Check the Lender Website Carefully 🌐

A legitimate lender website usually contains operational transparency.

What a Legitimate Lending Website Normally Shows

Borrowers should expect:

- Corporate disclosures

- Privacy notices

- Loan terms

- Interest explanations

- Data usage policies

- Customer support channels

Professional fintech operations also explain:

- ID verification steps

- Repayment methods

- Late payment handling

- Collection policies

Red Flags That Suggest Higher Risk

Be cautious if the site:

- Has no HTTPS security

- Uses copied content

- Hides corporate ownership

- Contains spelling inconsistencies

- Uses fake countdown timers

- Promotes “install outside app stores”

A borrower receiving an APK download link through SMS or Messenger should slow down immediately.

APK-based distribution bypasses normal app store review systems and increases malware exposure risk.

What to Do if the App Name Does Not Match the SEC Name

This is one of the most common borrower concerns.

Why Different Names Exist

Fintech companies often use:

- Marketing brand names

- Separate operating entities

- White-label platforms

This alone is not proof of illegality.

However, the relationship should still be transparent.

Borrowers should verify:

- The brand discloses the legal operator

- The privacy policy names the same entity

- Customer support confirms the relationship

- The company website references the app

When Mismatch Becomes Dangerous

Risk increases when:

- No explanation exists

- Multiple company names appear randomly

- The support team avoids answering

- The website domain differs entirely

- The SEC-listed entity has unrelated business activity

A legitimate lender normally clarifies the relationship quickly.

How the NPC Complaint Portal Helps Borrowers

The Philippines’ growing digital lending ecosystem also increased privacy-related complaints.

The National Privacy Commission complaint mechanisms became important because some lenders previously engaged in:

- Unauthorized contact access

- Public shaming tactics

- Excessive collection messaging

- Contact list scraping

Signs of Aggressive Data Practices

Borrowers should avoid apps requesting:

- Full contact list access

- Gallery permissions unrelated to KYC

- SMS reading access without justification

- Microphone permissions unrelated to onboarding

Loan App Permission Risks on Android Devices

(Android loan app permissions showing risks related to contacts, SMS, gallery, and device access)

The anchor topic loan app permissions risks matters because data abuse often starts during installation.

Modern fintech onboarding usually requires:

- Camera access

- ID upload

- Selfie verification

But many legitimate lenders no longer require unnecessary device-wide permissions.

Why Permission Auditing Matters

Permission abuse creates long-term privacy exposure.

A removed app may still:

- Retain borrower data

- Continue collections

- Share information with third parties

This is why verification should happen before ID upload, not after approval.

Fake Loan App Warning Signs 🚨

The phrase fake loan app warning signs should not be reduced to a simple checklist. Many fraudulent operators imitate legitimate fintech behavior convincingly.

Still, several operational patterns repeatedly appear.

High-Risk Behaviors to Watch

Be cautious when an app:

- Sends APK links through SMS

- Uses pressure tactics

- Threatens immediate legal action

- Requests advance processing fees

- Has no customer hotline

- Avoids corporate disclosure

- Promotes “instant approval without checks”

Suspicious Collection Practices

Another major warning sign appears after application submission.

Some problematic apps:

- Contact borrowers through personal numbers

- Threaten social media exposure

- Message unrelated contacts

- Change repayment instructions suddenly

Responsible digital lenders usually maintain:

- Official payment channels

- Transparent due dates

- Documented collection procedures

What Happens When Apps Disappear After Approval?

Some borrowers experience this:

- They receive loan approval

- The app disappears from the Play Store

- Customer support becomes unreachable

- Collection messages continue elsewhere

This creates confusion because app removal does not automatically erase existing borrower obligations or stored personal data.

Why Apps Get Removed

Possible reasons include:

- Policy violations

- Consumer complaints

- Security concerns

- Privacy issues

- Regulatory scrutiny

Why Borrowers Should Preserve Records

Before borrowing:

- Save screenshots

- Download repayment schedules

- Record company disclosures

- Keep official receipts

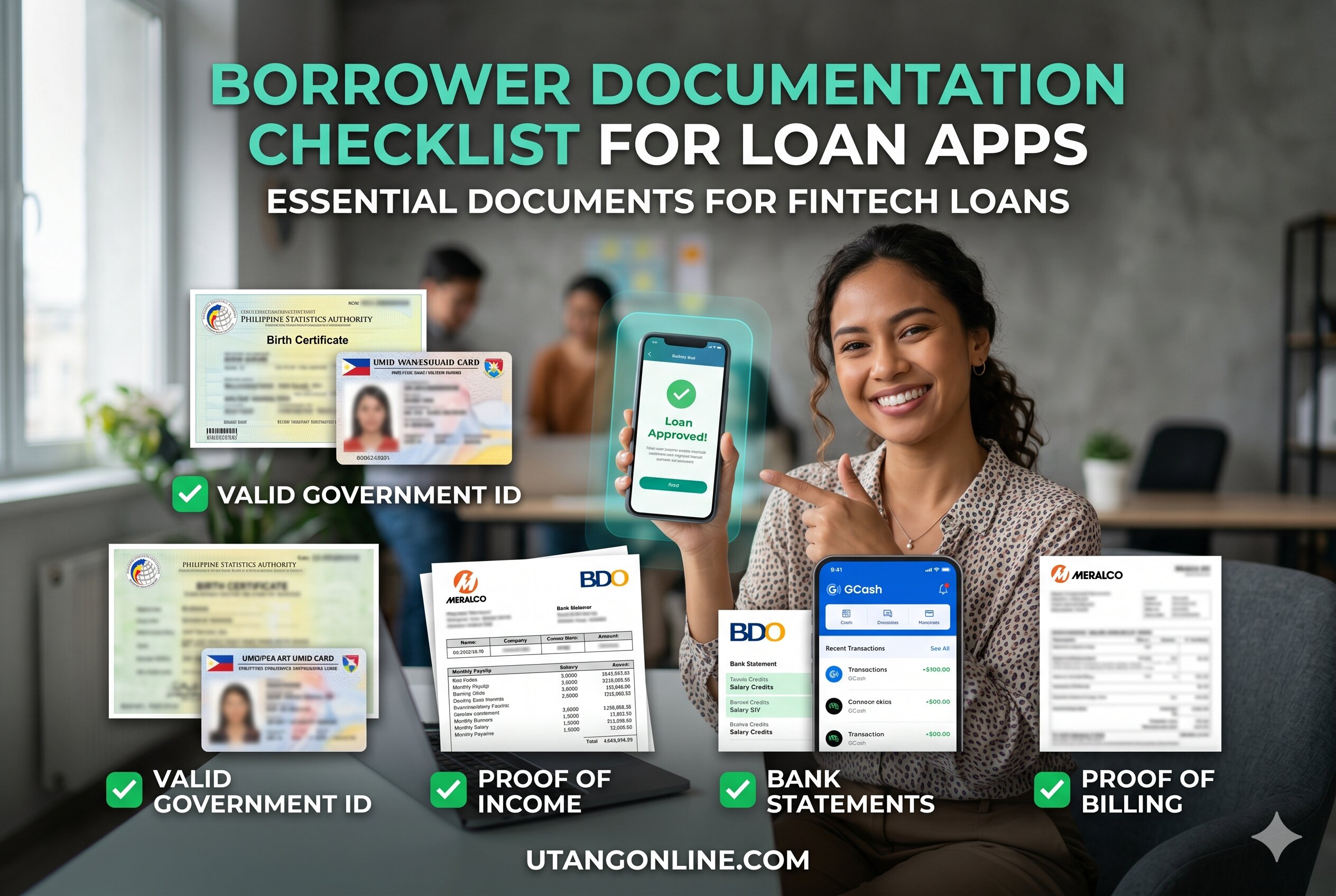

Borrower Documentation Checklist for Loan Apps

(Checklist showing screenshots, repayment records, SEC details, and support contacts for Philippine loan apps)

This helps borrowers protect themselves if:

- The app vanishes

- Payment disputes occur

- Collection behavior escalates

- Contact information changes suddenly

Practical Verification Checklist Before Submitting IDs

Here is a quick-reference workflow optimized for featured snippets and AI extraction.

10-Step Verification Checklist

- Identify the app’s legal company name

- Search the SEC database for the entity

- Compare the website and app disclosures

- Check if the privacy policy is accessible

- Inspect app permissions carefully

- Avoid APK-only download links

- Review customer complaints patterns

- Verify support channels and office details

- Save screenshots before applying

- Never upload IDs until verification is complete

This process helps reduce:

- Scam exposure

- Identity theft risk

- Harassment-related problems

- Fraudulent debt collection disputes

SEC Authority Explained for Borrowers

The anchor topic SEC authority explained matters because many borrowers think all online lenders are regulated the same way.

They are not.

What Borrowers Should Know

Different entities may operate as:

- Lending companies

- Financing companies

- Technology platforms

- Marketing intermediaries

Borrowers should focus on:

- Operational transparency

- Lending disclosures

- Corporate accountability

- Data privacy behavior

Why Verification Is Now Part of Safe Borrowing

Digital lending relies heavily on:

- Remote onboarding

- Electronic KYC

- Device verification

- Fraud scoring

- Behavioral risk models

Because applications happen remotely, borrower-side verification became essential.

A few minutes of checking can prevent:

- Identity misuse

- Fake repayment claims

- Illegal collection tactics

- Exposure of personal contacts

FAQs

Where can I verify SEC loan apps in the Philippines?

Borrowers can verify the operating company through SEC records, lender disclosures, app store information, and official websites. The most important step is matching the app brand with the actual corporate entity behind the lending service.

What if the company name is different from the app name?

This can be normal in fintech operations. However, the relationship between the app brand and legal entity should be clearly disclosed in the privacy policy, website, and support documentation.

Are Play Store apps automatically legal?

No. App stores review apps for platform compliance, but listing approval does not guarantee Philippine lending compliance or responsible data practices.

Can removed apps still operate?

Yes. Some lenders continue collections or communications after app removal. Borrowers should keep screenshots, repayment records, and official transaction receipts.

Is an APK loan app safe?

Borrowers should be cautious with APK-only distribution. Apps installed outside official app stores bypass standard marketplace screening and may carry higher security risks.

Why do loan apps request permissions?

Some permissions support identity verification and fraud prevention. However, excessive requests involving contacts, SMS access, or gallery access may indicate elevated privacy risk.

Safer Borrowing Habits Before Using Loan Apps

Borrowers can reduce risk significantly by adopting a few operational habits.

Before Applying

- Verify the legal entity

- Read privacy disclosures

- Review repayment structure

- Inspect permissions carefully

Before Uploading IDs

- Confirm website legitimacy

- Save lender disclosures

- Avoid rushed applications

- Double-check customer support channels

Before Accepting a Loan

- Review total repayment amount

- Check due dates carefully

- Avoid borrowing beyond repayment capacity

This matters especially for:

- Freelancers with irregular income

- Gig workers using e-wallet payouts

- First-time digital borrowers

- Users applying during financial emergencies

Conclusion

Loan apps in the Philippines continue to evolve alongside mobile banking, e-wallet usage, and digital identity verification. That convenience also means borrowers must become more careful before sharing IDs, contacts, and financial information.

The safest approach is verification before application. Checking the lender’s corporate identity, comparing app store disclosures, reviewing permissions, and matching information across the SEC database and official websites can reduce exposure to scams and abusive operators.

Borrowers should never assume that a polished app interface guarantees legitimacy. Responsible borrowing starts with careful validation, realistic repayment planning, and protecting personal data as seriously as money itself.

Last Updated on May 18, 2026 by Michael Reyes