Many fraudulent lending apps in the Philippines pretend to be legal by copying SEC registration numbers, cloning fintech brand identities, and using fake approval promises. These scams often operate through APK downloads, Facebook Messenger offers, Telegram groups, SMS links, and phishing pages designed to steal personal information. Borrowers are commonly pressured into submitting IDs, contacts, selfies, and mobile access before any loan is released.

Summary:

Fake SEC registered loan apps in the Philippines use impersonation tactics to appear legitimate while collecting sensitive borrower data. Common warning signs include apps downloaded outside the Google Play Store, fake SEC numbers, cloned logos, aggressive collection threats before disbursement, and requests for full contact access immediately after installation. Borrowers can reduce scam risk by checking SEC and lending authorization details, avoiding APK installations, reviewing app permissions carefully, and refusing lenders that pressure users through SMS, Messenger, or Telegram. Verification behavior is now one of the most important borrower safety habits in the Philippine digital lending market.

Why Fake Loan Apps Continue to Spread in the Philippines 📱

The Philippine digital lending ecosystem has grown rapidly because borrowers increasingly rely on mobile-first financing. Gig workers, freelancers, online sellers, delivery riders, BPO employees, and self-employed borrowers often use digital lenders for emergency liquidity.

Unfortunately, scammers target this demand aggressively.

Fake lenders know many users search for:

- Fast approval

- No collateral loans

- Minimal requirements

- Emergency cash

- Instant disbursement

Fraud operators exploit urgency and financial stress. They imitate real fintech companies and falsely claim to belong to lists of legitimate SEC registered loan apps Philippines.

Some even use:

- Stolen SEC registration numbers

- Fake certificates

- Copied UI designs

- Cloned logos

- Fabricated borrower reviews

- AI-generated customer support chats

The result is a dangerous environment where illegal apps appear almost identical to legal lenders.

How Fake Loan Apps Pretend to Be SEC Registered

Illegal lenders rarely present themselves as obviously fake. Most operate like professional fintech brands during the first interaction.

They Copy Real Registration Details

One of the most common tactics involves using the SEC registration number of a completely unrelated business entity.

Borrowers often assume:

- “May SEC number sila”

- “Mukhang legal”

- “May website naman”

But a valid SEC business registration does not automatically mean the company is authorized for lending operations.

A legal digital lender usually needs:

- Corporate registration

- Lending authority or financing authority

- Privacy compliance practices

- Transparent collection policies

- Proper disclosure documents

Scam apps intentionally blur these distinctions.

This is why borrowers should always verify SEC registered loan apps carefully instead of trusting screenshots or app descriptions alone.

They Clone Existing Fintech Brands

Another growing fraud pattern involves impersonated fintech brands.

Scammers copy:

- Brand colors

- App icons

- Company names

- Customer service templates

- Website layouts

Some fake APK sites even mimic legitimate app download pages almost perfectly.

Borrowers searching through Facebook or TikTok ads may not notice subtle domain differences.

Examples include:

- Added hyphens in URLs

- Misspelled fintech names

- Different Play Store publisher names

- APK download redirects

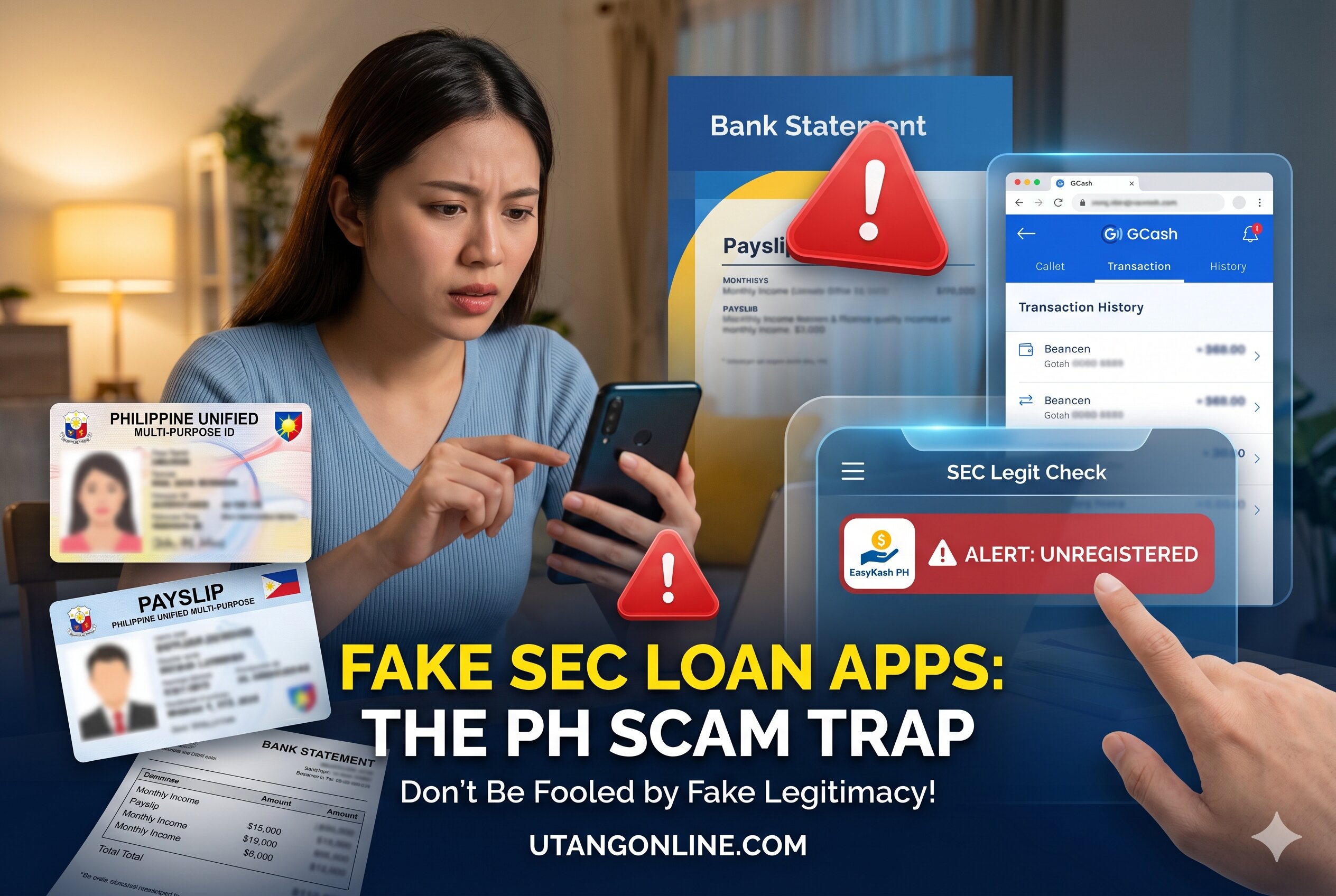

Fake Loan App Interface Mimicking Legal Philippine Lenders

(Fake SEC registered loan app in the Philippines copying fintech branding and approval screens)

The Most Dangerous Platforms Used by Scam Lenders

Fake lenders usually avoid transparent ecosystems where regulators and users can easily report abuse.

APK Download Websites

Legitimate lending apps are usually distributed through official app marketplaces with security screening layers.

Scam lenders frequently push borrowers toward:

- APK files

- Direct download links

- Unknown installer pages

This bypasses normal security checks.

Once installed, malicious apps may:

- Read SMS messages

- Access contacts

- Capture device information

- Monitor location data

- Extract photos or files

Many victims do not realize they granted these permissions.

Facebook Messenger Loan Offers

Messenger remains one of the most abused channels for fake loan promotions.

Common messages include:

- “Guaranteed approval”

- “No income proof needed”

- “Instant release today”

- “Bad credit accepted”

The conversation often moves quickly toward:

- ID submission

- Face verification

- Contact list access

- Advance fee requests

Fraudsters exploit emotional urgency, especially among borrowers facing overdue bills or salary gaps.

Telegram Lending Groups

A growing number of fake lenders now operate through Telegram.

This is a major red flag.

Legitimate lenders generally maintain:

- Official websites

- Registered customer support

- Transparent app listings

- Traceable business channels

Telegram-based lending offers are difficult to trace and frequently disappear after collecting borrower data.

This explains why many users ask:

Are Telegram Loan Offers Legal?

Most legitimate Philippine digital lenders do not process official consumer lending entirely through Telegram chats.

Scam operators favor Telegram because:

- Accounts are disposable

- Groups disappear quickly

- Identity verification is weak

- Complaints are harder to track

Borrowers should treat Telegram-only lenders with extreme caution.

Behavioral Red Flags That Reveal Fake Loan Apps 🚩

Scam detection is no longer only about checking logos or registration screenshots. Behavioral patterns are often more revealing.

They Demand Excessive Permissions Immediately

One major warning sign appears during app installation.

If a lender instantly requests:

- Full contact access

- SMS access

- Photo gallery access

- Call logs

- Device administrator permissions

before explaining why, borrowers should stop immediately.

Legitimate lenders may require limited identity verification for KYC compliance, but excessive permission harvesting is a common abuse tactic.

This is especially dangerous because some fake apps later use:

- Contact shaming

- Threat messages

- Edited photos

- Harassment campaigns

This is why many borrower complaints escalate into privacy violations.

They Threaten Borrowers Before Loan Release

A legal lender normally follows a structured process:

- Application

- Verification

- Risk assessment

- Approval or rejection

- Disbursement

- Repayment schedule

Scam lenders often skip operational logic entirely.

Some victims report receiving:

- Collection threats

- Public shaming warnings

- Penalty notices

before funds were ever disbursed.

This behavior strongly indicates fraud.

They Create Extreme Urgency

Scammers pressure borrowers emotionally.

Common manipulation tactics include:

- “Offer expires in 10 minutes”

- “Limited slots only”

- “Release today only”

- “Submit contacts now”

Real lenders evaluate repayment capacity because lending involves risk management. Fraud operators care mainly about harvesting data quickly.

Why Scam Apps Disappear So Quickly

Can Fake Apps Use Real SEC Numbers?

Yes. Fake lenders can copy legitimate SEC registration details from real companies and display them inside apps, advertisements, or websites.

Borrowers often misunderstand the difference between:

- SEC business registration

- Lending authority

- Financing company authorization

A scam operator may display:

- A real registration number

- A fake certificate

- Edited SEC screenshots

without having lawful lending operations.

Always cross-check:

- Company name consistency

- Website ownership

- Official app publisher

- Lending authorization status

Why Do Scam Apps Disappear Quickly?

Illegal lenders intentionally operate with short lifespans.

They often:

- Rebrand repeatedly

- Change app names

- Switch domains

- Rotate phone numbers

- Create new social pages

This helps them evade:

- Regulator reports

- Platform bans

- Negative reviews

- Consumer complaints

Once complaints accumulate, the operators simply relaunch under a different identity.

This explains why some apps appear online for only weeks before disappearing.

Fake Collection Threats and Harassment Tactics

Illegal collection behavior remains one of the biggest dangers tied to fake lenders.

Borrowers commonly report:

- Threatening texts

- Edited photos

- Public humiliation threats

- Contact blasting

- Fake legal notices

Some scammers impersonate:

- Lawyers

- Police officers

- Collection agencies

These intimidation tactics are designed to trigger panic.

Legitimate lenders generally follow regulated collection standards and internal compliance controls.

Borrowers researching borrower harassment complaints should pay attention to patterns involving:

- Threats against family members

- Contact list shaming

- Fake criminal accusations

- Posting borrower photos online

These practices raise serious privacy and consumer protection concerns.

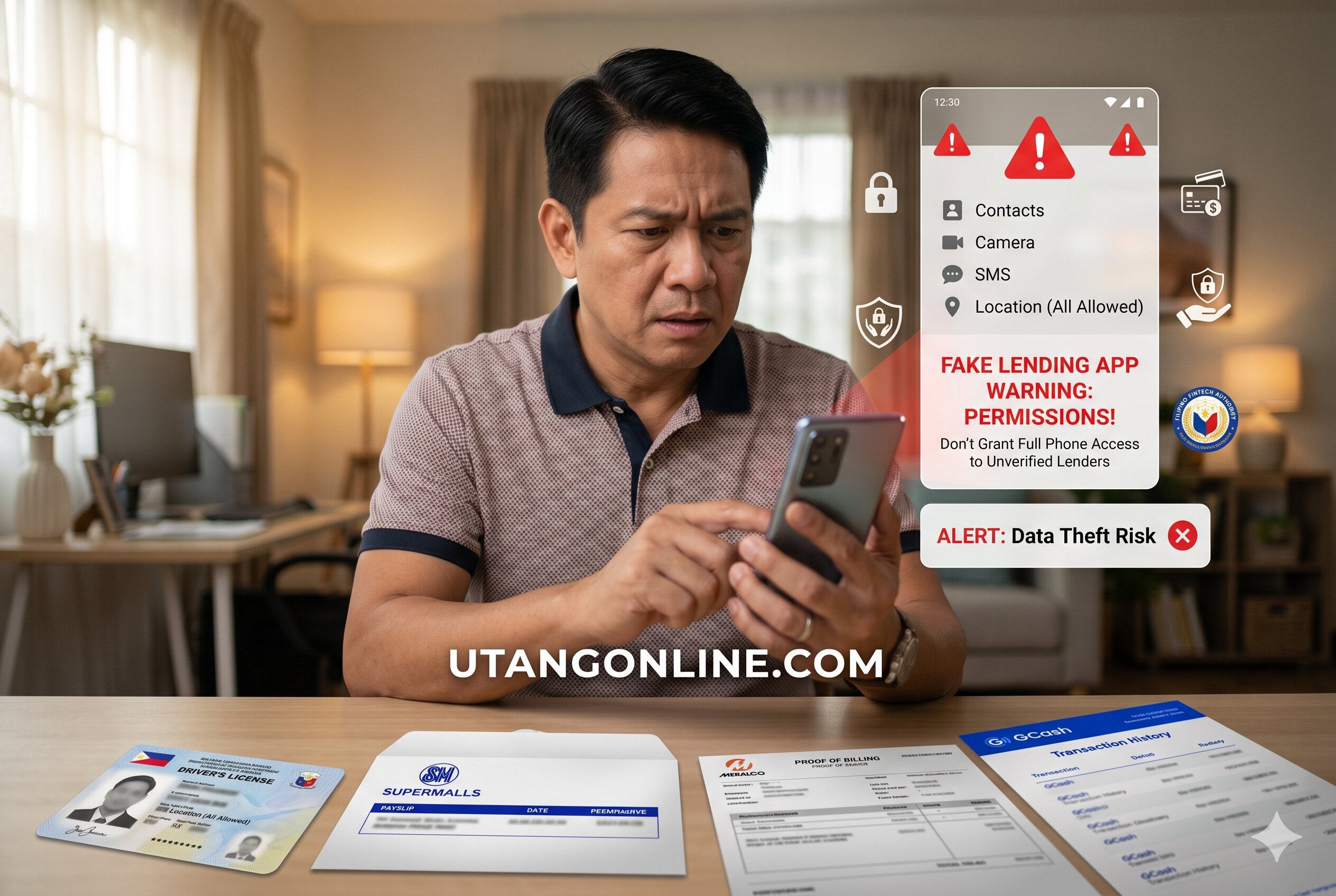

Smartphone Warning About Fake Lending App Permissions

(Dangerous loan app requesting contacts SMS and gallery permissions from Philippine borrower)

What Happens After You Submit Personal Information

Many borrowers believe the danger ends if they stop borrowing before disbursement. Unfortunately, identity exposure may already have occurred.

Fake lenders frequently collect:

- Government IDs

- Selfies

- Mobile numbers

- E-wallet details

- Employer information

- Address data

- Emergency contacts

This data can later be used for:

- Identity theft

- Social engineering

- SIM registration abuse

- Phishing attacks

- Fake account creation

Some scam operations even sell borrower databases to other fraud groups.

This is why early detection matters.

Practical Ways to Verify a Lending App Before Applying ✔️

Verification behavior is now essential for Filipino borrowers.

Check the App Distribution Source

Safer practices include:

- Downloading only from official app stores

- Reviewing developer names carefully

- Avoiding APK links from social media

Borrowers should avoid apps distributed purely through:

- Messenger

- Telegram

- Random SMS links

Examine Permission Requests

Pay attention to:

- Why permissions are requested

- Whether permissions match loan processing needs

- Timing of access requests

Immediate contact harvesting is a major warning sign.

Compare Official Branding Carefully

Check for:

- Website inconsistencies

- Grammar issues

- Different logos

- Fake reviews

- Unusual customer service behavior

Cloned fintech brands often reveal small inconsistencies.

Look for Regulatory Warnings

Borrowers should also monitor lists of:

- apps banned or removed by regulators

- SEC advisories

- Privacy violation complaints

Many scam apps repeatedly appear in consumer warning discussions before disappearing again.

What Legitimate Digital Lending Usually Looks Like

Not all online lenders are scams. However, legal lenders typically follow more structured operational processes.

Real Lenders Perform Structured KYC

Legitimate lenders generally:

- Explain data collection clearly

- Use structured onboarding

- Provide disclosure statements

- Present repayment schedules

- Maintain traceable support channels

KYC procedures may vary depending on:

- Employment type

- Income source

- Borrower risk profile

For example:

- Salaried employees may submit payslips

- Freelancers may provide bank activity

- Online sellers may show e-commerce income

- Gig workers may present platform earnings

Scam apps usually skip realistic risk assessment logic entirely.

Legitimate Lenders Care About Repayment Capacity

Real lenders evaluate:

- Income stability

- Existing obligations

- Identity consistency

- Fraud indicators

Fraud operators focus mainly on:

- Data extraction

- Fear manipulation

- Rapid user acquisition

This difference becomes visible during the application process.

Safe Loan App Verification Checklist for Philippine Borrowers

(Checklist for verifying SEC registered loan apps in the Philippines safely)

What If an App Asks for All Contacts Immediately?

This is one of the strongest warning indicators.

Some contact access may be requested for fraud prevention or device verification purposes, but immediate unrestricted harvesting raises serious concerns.

Borrowers should ask:

- Why is this necessary?

- Is the request proportional?

- Is there a privacy explanation?

- Can the application continue without full access?

Apps demanding excessive permissions before verification may expose users to:

- Contact harassment

- Social pressure collection

- Privacy abuse

When in doubt, stop the application.

The Emotional Psychology Behind Loan App Scams

Scam lenders rarely rely only on technology. They exploit emotional vulnerability.

Common emotional triggers include:

- Salary delays

- Medical emergencies

- Tuition stress

- Debt pressure

- Rejected bank applications

Fraudsters understand that desperate borrowers are less likely to verify legitimacy carefully.

This is why emotional manipulation appears repeatedly in:

- “Guaranteed approval”

- “No rejection”

- “Instant release”

- “No documents needed”

Real lending systems involve risk evaluation. No legitimate lender can guarantee approval to every borrower instantly.

How Borrowers Can Reduce Scam Exposure

Safer borrowing habits include:

Slow Down the Application Process

Scammers rely on rushed decisions.

Before applying:

- Review permissions

- Check company identity

- Search complaint patterns

- Verify official channels

Separate Urgency From Legitimacy

Emergency financial needs do not make a lender trustworthy.

A polished app interface does not guarantee:

- Legal authority

- Data protection

- Ethical collection behavior

Protect Personal Documents Carefully

Avoid uploading IDs unless:

- The lender identity is verified

- The app source is legitimate

- The company is traceable

Identity documents are highly valuable to fraud groups.

Frequently Asked Questions

Can fake apps use real SEC numbers?

Yes. Scam apps sometimes copy legitimate SEC registration details from unrelated companies to appear credible. Borrowers should verify whether the lender itself has lawful lending authority and consistent business identity.

Why do scam apps disappear quickly?

Fraud operators frequently change app names, domains, social media pages, and branding to avoid complaints, bans, and enforcement actions.

Are Telegram loan offers legal?

Telegram-only lending operations are high-risk because they are difficult to verify and trace. Legitimate lenders usually maintain official websites, regulated app listings, and transparent customer support channels.

What if an app asks for all contacts immediately?

Immediate unrestricted contact access is a major warning sign. Excessive permission harvesting may later be used for harassment or privacy abuse.

Are apps outside the Play Store dangerous?

Not always, but APK-only lending apps carry significantly higher risks because they bypass official marketplace screening and security controls.

Conclusion

Fake SEC registered loan apps in the Philippines continue to evolve by copying legitimate fintech branding, impersonating legal lenders, and exploiting borrower urgency. Many victims only realize the danger after submitting IDs, contacts, selfies, or sensitive financial data.

Safer borrowing starts with verification behavior. Borrowers should carefully review app permissions, avoid APK installations from untrusted sources, verify lender legitimacy beyond screenshots, and remain cautious of Messenger or Telegram loan offers.

Financial emergencies can create pressure, but rushing into unverified lending apps increases the risk of identity theft, harassment, and long-term privacy exposure. Responsible digital borrowing means slowing down, validating lender credibility, and prioritizing data protection before submitting any personal information.

Last Updated on May 18, 2026 by Michael Reyes