Many borrowers assume that once a loan app is registered with the Philippine Securities and Exchange Commission (SEC), collectors can legally pressure them in any way they want. That is false. Even SEC-registered online lenders must follow strict rules on debt collection ethics, borrower privacy, and fair treatment. Harassment, public shaming, threats of arrest, and unauthorized contact with relatives may violate SEC rules, data privacy laws, and consumer protection standards.

Borrowers experiencing intimidation from digital lending apps often feel trapped because collectors use emotional pressure, repeated calls, social embarrassment, or fear tactics. However, Philippine borrowers still have enforceable rights, even when they have unpaid balances. Knowing those rights can help reduce panic and prevent abusive collection practices from escalating.

Summary:

Borrowers dealing with abusive collection tactics from online lenders have legal protections under Philippine regulations. The topic of borrower rights SEC registered loan apps Philippines covers harassment limits, privacy rights, complaint procedures, and ethical debt collection standards enforced by the SEC and other regulators. SEC-registered lending apps cannot legally threaten arrest, publicly shame borrowers, post personal information online, or aggressively contact unrelated third parties. Borrowers should preserve screenshots, call logs, payment records, and collector messages as evidence. Complaints may be filed with the SEC, National Privacy Commission (NPC), or other authorities depending on the violation. Even legitimate lenders must comply with ethical collection standards and borrower data protection obligations.

Why Borrowers Feel Intimidated by Loan App Collection Practices 😟

Digital lending in the Philippines expanded rapidly because of mobile-first onboarding, e-wallet integration, and simplified KYC verification systems. Many borrowers apply through apps using:

- Government IDs

- Selfie verification

- Mobile number authentication

- Device permissions

- E-wallet accounts

- Salary or income details

These onboarding systems help lenders assess risk quickly. However, some collection agents misuse access to borrower information after repayment delays occur.

The emotional pressure becomes stronger because many borrowers:

- Fear damage to their reputation

- Worry relatives or coworkers will be contacted

- Assume collectors can file criminal cases immediately

- Do not know where to report abusive behavior

- Confuse legal collection efforts with harassment

A loan default is generally a civil matter, not an automatic criminal offense. That distinction matters because abusive collectors often rely on fear rather than lawful recovery procedures.

What SEC-Registered Loan Apps Are Allowed to Do

Being late on a loan does not erase the lender’s right to collect payment. Legitimate lenders can still:

- Send payment reminders

- Call borrowers during reasonable hours

- Offer restructuring or repayment arrangements

- Notify borrowers about penalties stated in contracts

- Escalate unpaid accounts through lawful collection channels

However, ethical collection standards require professionalism and respect for borrower privacy.

Legitimate Collection Behavior

Professional collection teams usually:

- Identify themselves properly

- Explain the outstanding balance clearly

- Avoid profanity or humiliation

- Limit contact frequency

- Follow documented collection workflows

- Maintain records of borrower communication

Legitimate fintech lenders also tend to maintain internal compliance teams because SEC oversight and reputational risks affect their operations.

Illegal or Abusive Collection Practices

Collection behavior may become abusive when agents:

- Threaten arrest without legal basis

- Use vulgar or degrading language

- Send threats to relatives or employers

- Access unauthorized contact lists

- Post borrower information publicly

- Use edited photos or social media shaming

- Pretend to be law enforcement

- Call repeatedly late at night

- Harass emergency contacts unrelated to the debt

These practices may violate SEC memorandum circulars, privacy regulations, and consumer protection expectations.

Borrower Receiving Threatening Loan Collection Messages

(Filipino borrower reviewing threatening collection texts from a digital loan app)

Can Loan Apps Contact Your Relatives or Friends?

This is one of the most searched concerns among distressed borrowers in the Philippines.

The answer depends on the purpose and extent of contact.

Limited Verification vs Harassment

Some lending apps request references or emergency contacts during onboarding. Legitimate lenders may verify identity or attempt limited contact if they cannot reach the borrower. However, that does not automatically authorize harassment.

Collectors generally should not:

- Repeatedly spam relatives

- Reveal confidential debt details publicly

- Pressure unrelated contacts to pay the debt

- Humiliate borrowers through group messages

- Spread allegations on social media

Once collection efforts target embarrassment instead of repayment communication, the behavior may cross into harassment territory.

Unauthorized Access to Contact Lists

Some abusive apps previously requested broad phone permissions that allowed access to entire contact lists. Complaints arose when collectors messaged dozens of contacts after missed payments.

This is one reason borrowers should review app permissions carefully before installation. Checking safe loan app permissions helps reduce privacy exposure during the application process.

Modern compliance expectations increasingly emphasize:

- Data minimization

- Explicit consent

- Transparent processing

- Limited third-party disclosure

Apps that misuse borrower contacts risk complaints before the National Privacy Commission.

Is Public Shaming Legal? 🚫

Public shaming is one of the clearest red flags of abusive collection behavior.

Examples include:

- Posting borrower photos online

- Labeling someone a scammer publicly

- Editing humiliating images

- Sharing debt details in Facebook groups

- Sending mass messages to coworkers

- Threatening viral exposure

These tactics are widely criticized because they weaponize shame rather than lawful collection methods.

Privacy Rights Still Apply to Borrowers

Even if a borrower has unpaid debt, personal information remains protected.

Sensitive borrower information may include:

- Full name

- Mobile number

- Government IDs

- Home address

- Employment information

- Loan balances

- Photos

- Contact network

Public disclosure without lawful basis can trigger privacy complaints and regulatory scrutiny.

Why Legitimate SEC-Registered Lenders Avoid Public Shaming

Established lenders understand that aggressive harassment creates:

- Regulatory exposure

- Reputation damage

- Consumer complaints

- Platform delisting risks

- Negative media attention

That is why borrowers should distinguish between:

- Legitimate collection pressure

- Fake intimidation tactics

- Clearly abusive conduct

Some borrowers facing severe harassment later discover the lender was operating outside compliance expectations despite claiming legitimacy. Reviewing patterns associated with fake SEC loan app behavior can help borrowers identify warning signs earlier.

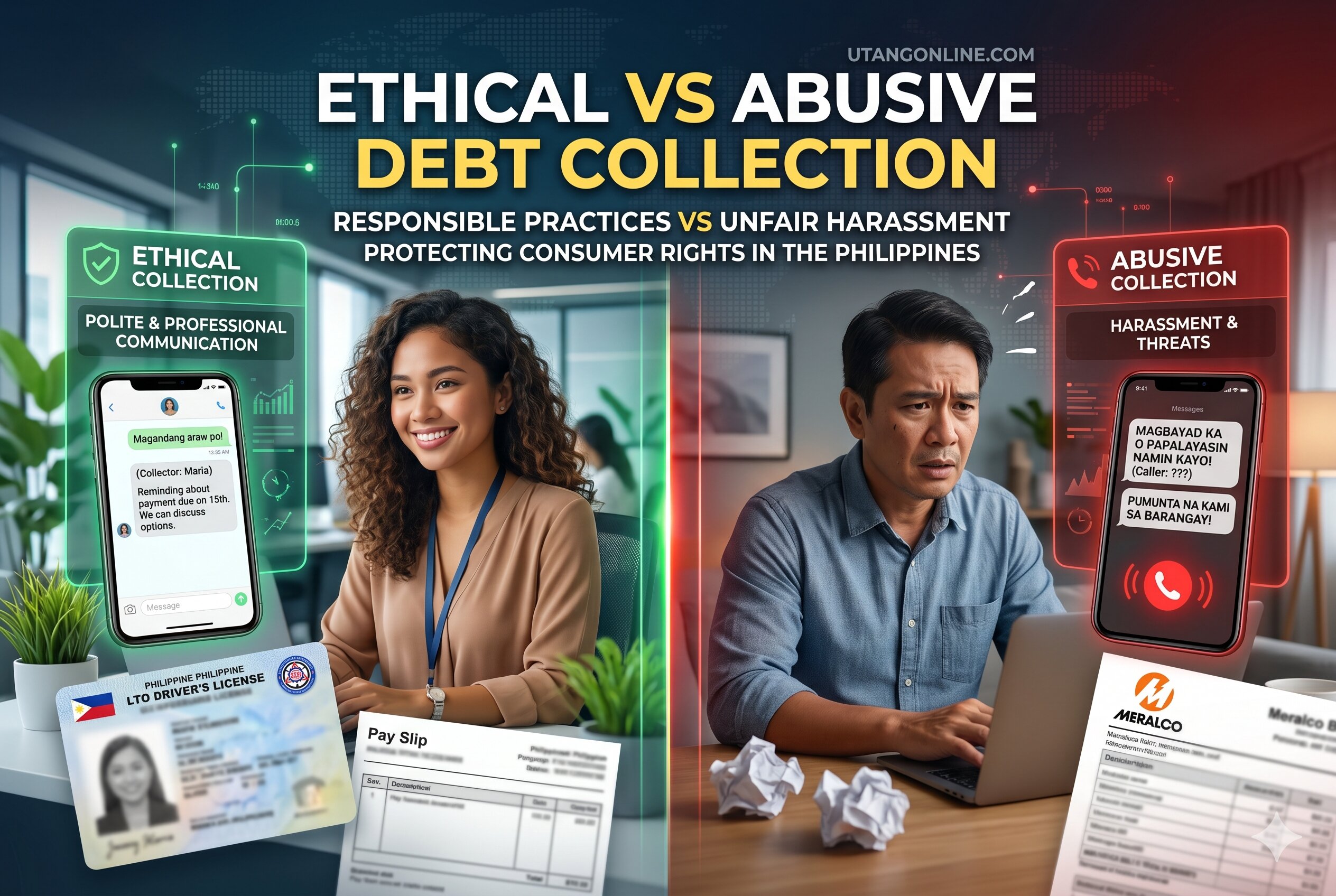

Example of Ethical vs Abusive Debt Collection Practices

(Comparison chart showing lawful debt collection versus illegal harassment from loan apps)

Can Collectors Threaten Arrest?

Collectors frequently use legal-sounding threats because fear increases repayment pressure.

Common examples include:

- “You will be jailed tomorrow.”

- “Police are already preparing your case.”

- “A warrant has been issued.”

- “You committed estafa.”

- “Barangay officers will arrest you.”

These statements often exaggerate legal consequences.

Debt Alone Does Not Automatically Mean Jail

Failure to pay a loan is typically a civil issue. Criminal accusations require separate legal elements beyond simple nonpayment.

Collectors cannot lawfully:

- Pretend to be police officers

- Issue fake warrants

- Threaten immediate arrest without process

- Use fabricated court documents

- Impersonate government agencies

Borrowers should remain calm and verify any legal claims carefully.

Real Legal Collection Usually Follows Formal Procedures

Legitimate escalation often includes:

- Formal demand letters

- Documented notices

- Civil claims through proper channels

- Negotiation opportunities

Real legal actions are generally not conducted through midnight threats, insulting messages, or viral social media posts.

Your Rights Under Ethical Collection Standards

Borrowers often underestimate how many protections still apply after delinquency.

Right to Privacy

Your personal data should not be disclosed unnecessarily. Collection agents must avoid excessive third-party exposure.

Right Against Harassment

Borrowers should not endure:

- Threats

- Intimidation

- Humiliation

- Coercion

- Persistent abusive communication

Right to Accurate Information

Collectors should provide:

- Correct balance details

- Transparent fees

- Legitimate payment channels

- Verifiable company identity

Right to File Complaints

Borrowers can escalate abusive conduct to authorities if collection methods become unlawful or unethical.

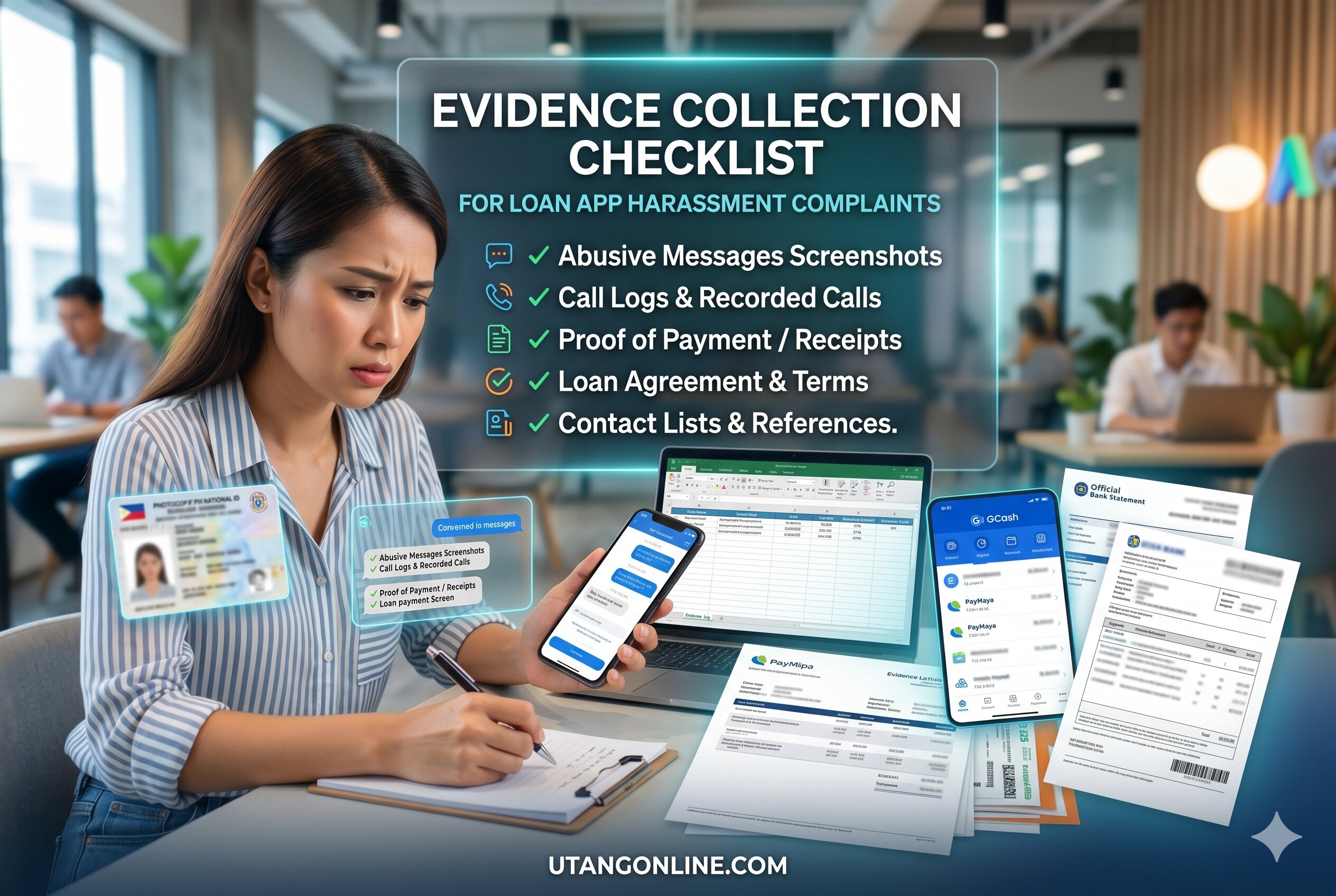

What Evidence Should You Save? 📱

Evidence collection matters because emotional distress alone may not fully establish violations.

Important Records to Preserve

Save:

- Screenshots of threats

- Chat conversations

- Call recordings if legally permitted

- Payment receipts

- Loan agreements

- Collection emails

- Social media posts

- Contact harassment messages

- Names of collection agents

- Dates and timestamps

Organizing evidence chronologically helps regulators evaluate complaints faster.

Why Borrowers Should Avoid Deleting Messages

Many borrowers delete messages out of panic or embarrassment. Unfortunately, this weakens documentation later.

Even partial evidence may help establish:

- Harassment frequency

- Public shaming

- Privacy violations

- False threats

- Unauthorized disclosure

Evidence Collection Checklist for Loan App Harassment Complaints

(Checklist of screenshots, call logs, and evidence needed for online loan harassment complaints)

Where to Report Abusive Loan Collection Practices

Different violations may involve different authorities.

SEC Complaints

The SEC may review:

- Lending compliance concerns

- Collection misconduct

- Violations involving lending operations

- Complaints against registered lenders

Borrowers searching for report abusive loan apps often start with SEC complaint channels when the lender claims registration status.

National Privacy Commission (NPC)

The NPC may handle:

- Unauthorized data sharing

- Contact list misuse

- Public disclosure of personal data

- Privacy breaches

Privacy complaints become especially relevant when collectors contact unrelated third parties or spread borrower information online.

Cybercrime or Law Enforcement Channels

Serious threats, impersonation, extortion-like behavior, or fake legal notices may justify escalation to additional authorities.

How Ethical Digital Lenders Usually Handle Delinquent Accounts

Not all lenders behave abusively. Many legitimate digital lenders follow structured risk management procedures.

Internal Risk Monitoring

Responsible lenders often:

- Segment overdue borrowers by risk level

- Automate reminder schedules

- Offer restructuring windows

- Monitor fraud indicators separately

- Maintain audit logs for collection calls

Professional operations avoid emotional escalation because regulators increasingly monitor consumer treatment standards.

Why Reputable Lenders Protect Borrower Privacy

Well-established fintech firms depend on:

- App store reputation

- Consumer trust

- Investor confidence

- Regulatory compliance

- Sustainable portfolio performance

Public harassment damages all of those objectives.

This is why borrowers researching SEC registered loan apps Philippines should also evaluate collection reputation, not just registration claims.

Warning Signs That Collection Conduct May Be Abusive

Certain behaviors strongly suggest potential violations.

Red Flags Borrowers Should Take Seriously

Watch for:

- Threats of immediate imprisonment

- Social media humiliation

- Fake legal documents

- Repeated calls to unrelated contacts

- Vulgar insults

- Deeply personal attacks

- Edited defamatory images

- Pressure to borrow elsewhere to repay

- Threats involving employers or schools

Emotional Manipulation Tactics

Collectors sometimes exploit:

- Family pressure

- Workplace embarrassment

- Religious guilt

- Fear of public exposure

- Panic over legal terminology

Recognizing these tactics helps borrowers respond more rationally instead of reacting emotionally.

What Borrowers Should Do During Active Harassment

Panic often leads to poor decisions, including borrowing repeatedly from multiple apps.

Immediate Actions That Help

- Stop responding emotionally to threats

- Preserve all evidence

- Verify whether the lender is truly registered

- Request written account details

- Avoid sharing new sensitive information

- Review payment history carefully

- File complaints when necessary

- Seek legitimate repayment arrangements if possible

Avoid These Risky Reactions

Do not:

- Share OTPs

- Install unknown remote-access apps

- Send additional IDs impulsively

- Pay through suspicious personal accounts

- Borrow repeatedly just to silence collectors temporarily

Repeated rollover borrowing often worsens debt stress.

Borrowers With Financial Hardship Still Have Rights

Many overdue borrowers are:

- Freelancers with irregular income

- Delivery riders

- Gig workers

- Commission-based earners

- Self-employed sellers

- Employees facing delayed salaries

Digital lenders already factor repayment risk into their underwriting systems. Delinquency alone does not justify humiliation or unlawful pressure.

Modern fintech risk models analyze:

- Income consistency

- Device patterns

- Repayment behavior

- Identity validation

- Fraud indicators

- Banking activity

- E-wallet usage

Because lenders knowingly operate in higher-risk lending segments, ethical collection remains essential.

Frequently Asked Questions

Can SEC-registered loan apps harass borrowers?

No. SEC registration does not allow lenders or collection agents to threaten, publicly shame, or unlawfully expose borrower information. Ethical collection standards still apply.

Can loan apps legally contact my relatives?

Limited contact may occur for verification purposes, but repeated harassment, humiliation, or unnecessary disclosure of debt information may violate privacy and ethical standards.

Is public shaming over unpaid loans legal?

Public shaming may violate borrower privacy rights and ethical collection expectations, especially when personal information or humiliating content is shared publicly.

Can collectors threaten me with arrest?

Collectors cannot lawfully issue fake warrants, impersonate police, or threaten immediate imprisonment purely because of unpaid debt.

What evidence should I keep?

Save screenshots, chat logs, call records, payment receipts, social media posts, and collector details. Evidence strengthens regulatory complaints.

How do I know if a lender is legitimate?

Check SEC registration status, borrower reviews, collection behavior patterns, app permissions, and complaint history before borrowing.

Why This Topic Matters More Today

Digital lending has become deeply integrated into Philippine financial behavior because of:

- Smartphone adoption

- Instant onboarding

- E-wallet ecosystems

- Alternative credit scoring

- Faster approvals

At the same time, borrower complaints about harassment pushed regulators and consumers to pay closer attention to ethical collection practices.

Today, responsible lending is no longer judged only by approval speed. Borrowers increasingly evaluate:

- Transparency

- Privacy protection

- Collection ethics

- Complaint handling

- Permission requests

- Communication professionalism

That shift benefits both consumers and legitimate fintech operators.

Conclusion

Borrowers facing harassment from online loan apps should remember one critical fact: unpaid debt does not erase your rights. Even SEC-registered lenders must follow lawful and ethical collection standards. Threats, public humiliation, fake legal intimidation, and privacy violations may cross regulatory and legal boundaries.

Staying calm, preserving evidence, verifying lender legitimacy, and reporting abusive conduct are practical steps that protect borrowers from further harm. Responsible borrowing still matters, but ethical treatment matters too. As digital lending continues growing across the Philippines, stronger borrower awareness helps encourage safer fintech practices, healthier collection standards, and more accountable lending ecosystems.

Last Updated on May 18, 2026 by Michael Reyes